The S&P 500 Lost 28% Last Year and Nobody Noticed

How nominal gains mask a historic wealth transfer as central banks vote with their vaults

Your brokerage statement says you had a good year. The S&P 500 was up about 18% in 2025. If you were broadly indexed, you probably felt vindicated: another year where staying invested “worked.”

Then I measured the same year using a different ruler.

Against gold, that same S&P 500 performance was a 28% decline. One market, one year, two answers that can’t both feel true in your gut. The gap between the two is about 46 percentage points—the kind of gap that quietly rewires a society’s balance sheet without a single headline.

I kept coming back to a simple, uncomfortable thought: stocks aren’t necessarily getting cheaper. The ruler is shrinking. And when the ruler shrinks, the people who understand the game early don’t argue about narratives. They change what they hold.

That’s where the story gets interesting. Because while retail investors celebrated nominal gains, the people who run sovereign money were behaving as if something more structural is underway.

The Nominal Illusion

Most investors are trained to think in nominal terms because their lives are denominated in nominal terms. Salaries, mortgages, taxes, brokerage statements: they all speak dollars. So when the S&P 500 rises 18% in a year, the brain does what it’s supposed to do. It translates that into progress.

But markets don’t just move. They move relative to other things. And the most revealing comparison I found wasn’t S&P versus bonds, or growth versus value. It was stocks versus gold, because gold functions as a kind of monetary yardstick precisely because it isn’t someone else’s liability.

In 2025, the index was up about 18% in dollars but down 28% when measured against gold. That’s the contradiction that frames everything else.

The raw ingredients of the divergence are visible in plain sight. Gold rose roughly 60% to 65% in 2025 while the S&P 500 gained roughly 16% to 18%. If the thing you’re pricing stocks in is falling faster than stocks are rising, you can have a “great year” and still lose ground.

Zoom out and the pattern stops looking like a quirky one-year anomaly. On a five-year comparison using long-term market data, the S&P 500 was up about 88% versus the dollar, while gold rose about 180%. That’s a regime signal. It tells you the unit of account has been doing something unusual for long enough that it’s now shaping outcomes.

The cleanest way to see the structural change is the S&P-to-gold ratio—a simple measure of how many ounces of gold it takes to “buy” the index. In 2000, that ratio sat around 45 ounces. By 2026, it’s around 1.37 ounces.

That’s the kind of chart that makes you stop arguing about whether the S&P is “expensive” or “cheap.” If it used to take roughly 45 ounces of gold to buy the index and now it takes about 1.37, something profound happened in the measuring system. Either U.S. equities became historically worthless relative to gold, or gold became historically expensive relative to U.S. equities, or the currency unit in between lost credibility as a neutral yardstick. In practice, it’s some blend of all three. But the direction matters more than the purity.

Gold isn’t the only witness. Even within fiat currencies, the dollar’s relative motion in 2025 tells you the same story: down around 4% versus the yuan, down around 12% versus the euro, and down around 13% versus the Swiss franc. Gold is simply the harshest mirror because it doesn’t flatter anyone’s policy choices.

Here’s what I think most people miss: nominal returns are not returns. They’re movement within a measuring system. If the measuring system is being diluted, then “up 18%” can be the financial equivalent of running on a treadmill that’s accelerating beneath you.

That observation naturally raises the next question: why would the ruler shrink? Not as a conspiracy. As arithmetic.

The Arithmetic of Inevitability

If you want to understand why governments tolerate currency erosion, don’t start with ideology. Start with the balance sheet.

As of early January 2026, the U.S. national debt hit $38.43 trillion, according to the Joint Economic Committee. The same release pegged the year-over-year increase at $2.25 trillion, which works out to roughly $8.03 billion per day.

It’s hard to hold that number in your head. Eight billion a day isn’t “a lot.” It’s a different category of motion. It’s the kind of daily increment that would be a lifetime of capital formation for most people, and it’s being added as background noise.

Debt by itself isn’t the trap. The trap is what happens when the cost of carrying that debt rises while the political system remains allergic to austerity.

In FY 2025, net interest payments reached about $970 billion, according to the Committee for a Responsible Federal Budget. CRFB also projects net interest to surpass $1 trillion in FY 2026. When interest costs approach that scale, they stop being “a line item” and start behaving like a competing branch of government. They demand funding before anything else gets debated.

Another way to see the squeeze is to look at interest as a share of federal spending. Using the federal data series tracked through FRED, interest payments now consume roughly 15% to 17% of federal spending. That’s the quiet crowding-out effect: even if you don’t cut programs, you can still strangle them by letting interest eat the discretionary space.

Then 2025 delivered the refinancing problem in its purest form. About $9.2 trillion in Treasury maturities were refinanced in 2025 at higher interest rates. Cheap debt became expensive debt. Not because of a moral failure. Because that’s what happens when a long period of low rates collides with the calendar.

Once you internalize that, the menu of “solutions” gets smaller than the political rhetoric suggests.

In theory, a government facing a debt and interest spiral has three broad levers:

Raise taxes enough to stabilize the trajectory.

Cut spending enough to stabilize the trajectory.

Reduce the real burden of the debt by changing the value of the money used to repay it.

In practice, the first two levers are politically radioactive at the scale required. You can argue about which constituencies should take the pain, but the pain is the point. The numbers are too large to hide inside “efficiency” or “closing loopholes.” And when interest is already consuming 15% to 17% of spending, the required adjustments get more brutal over time, not less.

So the system drifts toward the third lever, because it’s the only one that can be implemented without a formal vote that explicitly assigns blame.

I don’t think most people appreciate how convenient currency devaluation is as a policy tool. It’s not framed as a tax, but it behaves like one. It reduces the real value of cash and fixed claims. It favors debtors over savers. And the largest debtor in the system is the sovereign itself.

Dalio’s Warning

Ray Dalio is interesting because he’s been directionally right about leverage cycles in moments when being right was expensive.

A profile of his track record notes that Bridgewater Associates profited $14 billion during the 2008 financial crisis after Dalio’s models flagged excessive leverage. That doesn’t make him infallible. But it does establish that he’s someone whose framework has survived contact with a real panic.

Dalio’s core claim about debt traps is blunt, and it matters because it turns moral arguments into mechanics. As he put it:

“If you devalue money, you devalue debt”

That line, from his warning about fiat currencies, is the cleanest explanation I’ve seen for why governments eventually lean on the currency. Debt is a promise to deliver future money. If the money is worth less, the promise is easier to keep.

Dalio has also framed the issue in more pointed terms when discussing monetary policy itself. In a January 2025 post, he asked:

“Can printing money solve everything? ... devalue money and debt assets”

The ellipsis matters because it’s not a neat slogan. It’s a thought in motion: the temptation to print, the short-term relief, and the long-term cost paid by holders of the currency and debt claims.

In his public positioning, Dalio doesn’t frame gold as a get-rich instrument. He frames it as a form of balance. The same warning that included his “devalue money” line also notes that Dalio recommends a 5% to 15% allocation to gold. That’s a call to hold something that behaves differently when the system’s failure modes activate.

What I find most useful in Dalio’s thinking is his insistence that the conflict evolves. Trade wars don’t stay trade wars. They become capital wars, and then they become something uglier.

If the debt arithmetic pushes governments toward devaluation, then the next question is whether sophisticated institutions behave as if that’s already the base case.

They do. And the most revealing actors aren’t hedge funds. They’re central banks.

Central Banks Vote With Their Vaults

Central banks are not retail investors with a hunch. They are the institutions tasked with managing national reserves, liquidity, and, in many cases, the credibility of the currency itself. They also have a peculiar incentive: they must publicly project stability even when privately preparing for instability. That’s the job.

Which is why their behavior matters more than their speeches.

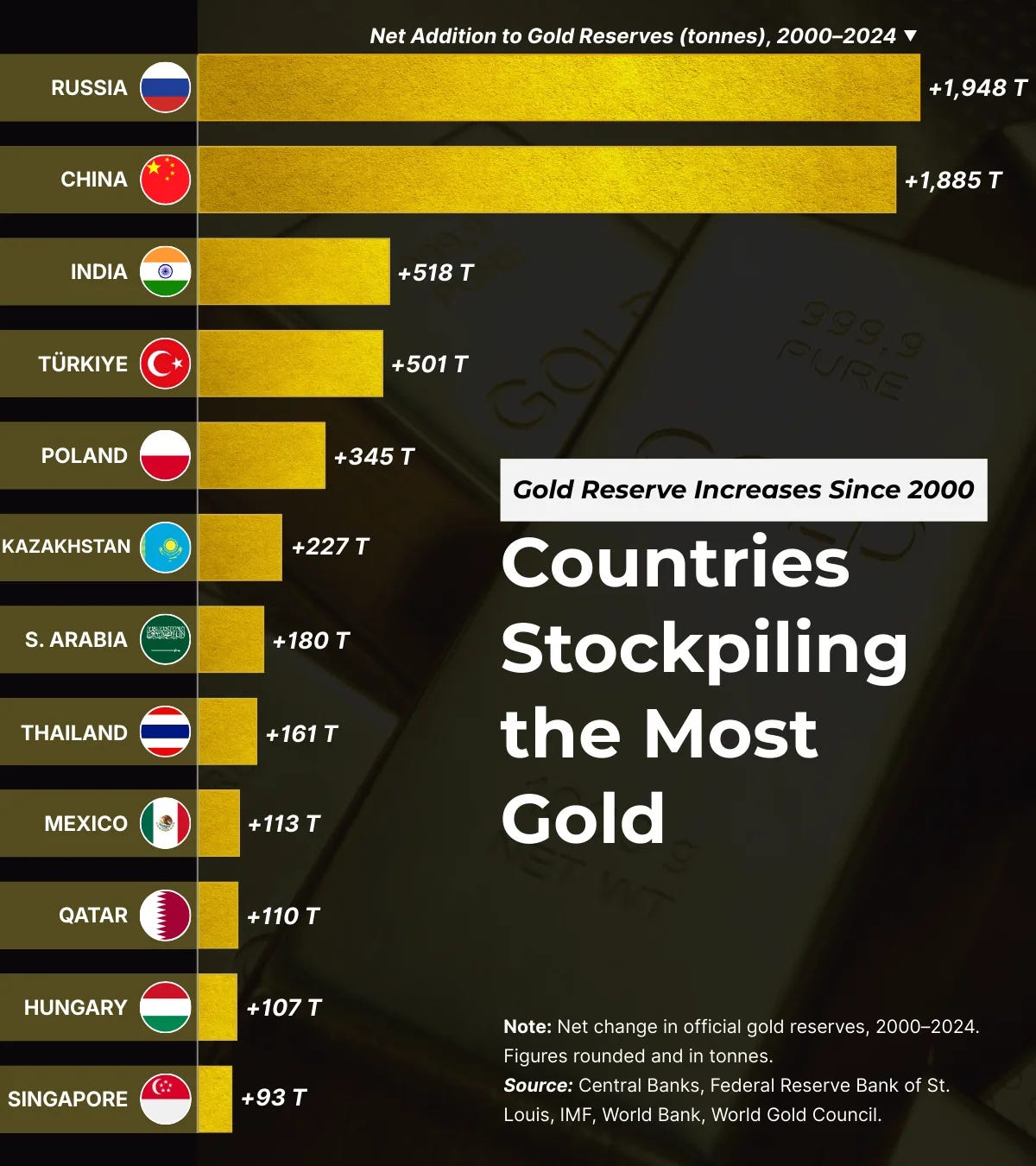

The World Gold Council reported that central banks bought 45 tonnes of gold in November 2025 alone, with buying momentum continuing. One month doesn’t define a trend. But the WGC’s framing is explicit: sustained demand from the very institutions that sit at the center of the monetary system.

The strategic shift shows up not only in flows, but in reserve composition. The WGC’s Central Bank Gold Reserves Survey 2025 notes that gold’s share of global central bank reserves has approximately doubled from about 4% to about 9% to 10%.

Doubling the share is a structural change in institutional preference. Central banks don’t double reserve allocations casually. They do it when the risk model changes.

The same WGC survey also found that 43% of central banks plan to increase their gold holdings further, and 73% expect a lower U.S. dollar share of reserves. That’s a remarkable pair of numbers because it captures both motive and direction. It’s “buy more gold” and “hold fewer dollars.”

Then there’s the country example that made me pause: Poland.

A market update highlighted that Poland’s gold reserves hit 543 tonnes, representing 28% of total reserves. Twenty-eight percent is not a marginal hedge. Poland sits on NATO’s eastern flank. It lives with the reality that geopolitics can change quickly. And it has chosen to hold nearly a third of its reserves in an asset that is not someone else’s promise.

China’s posture reinforces the pattern at scale. China holds 2,303 tonnes of gold and has been buying monthly, according to Trading Economics. China doesn’t buy gold because it likes shiny objects. It buys gold because it understands that reserves are political instruments as much as financial ones.

Here’s the tension: central banks publicly support dollar stability while privately increasing gold holdings and anticipating a lower dollar share of reserves. If you only listen to the speeches, you miss the vote. The vote is in the vault.

And Poland’s allocation hints at something beyond debt dynamics. It points to a world where reserves aren’t just about returns. They’re about survivability in a system where money can be weaponized.

That brings us to the event that changed the risk calculus for every sovereign with dollars in custody.

Capital Wars

In 2022, after Russia’s invasion of Ukraine, approximately $300 billion in Russian sovereign assets were frozen, as described by the Brookings Institution. The number itself is staggering, but the more important detail is what the freeze demonstrated.

It demonstrated that reserve assets are conditional. Access can be revoked.

That might sound obvious in a world where sanctions have existed for decades. But there’s a difference between sanctioning individuals and showing that a major power’s sovereign reserves can be immobilized at scale. It forced a question onto the desks of finance ministries everywhere: If it can happen to them, can it happen to us?

The dollar’s dominance has long been reinforced by the idea that it is the world’s safest asset base. But safety is not only about credit risk. It’s also about political risk. And political risk is the one variable that can change overnight.

Once you accept that, the logic of building parallel infrastructure becomes straightforward. Countries that anticipate conflict with U.S. interests have incentives to reduce exposure to U.S.-controlled financial plumbing.

China’s Cross-Border Interbank Payment System, CIPS, processes approximately RMB 170 trillion annually. The point isn’t that CIPS has replaced SWIFT. The point is that the scale is already large enough to matter. Parallel rails exist, and they’re being used.

Russia has its own SPFS system. China has CIPS. The existence of these systems changes the bargaining dynamics even if they don’t fully displace the incumbent. They reduce the cost of defection.

Then there’s the BRICS experiment. Late 2025 saw a pilot of a digital settlement tool described as a “Unit,” characterized as 40% gold-backed and 60% BRICS currencies. I’m careful here because pilot programs are not regimes. The honest answer is that nobody knows yet whether this moves from pilot to an operational currency-like instrument. But the direction is what matters: an attempt to build settlement that is less exposed to dollar infrastructure and more anchored to something harder.

The scale of the potential bloc is not trivial. The WGC survey notes that BRICS nations represent nearly half the world’s population and over a third of global GDP. That doesn’t mean they can snap their fingers and dethrone the dollar. It does mean that experimentation with non-dollar settlement has a large addressable base.

Dalio has been explicit about where this trajectory can lead. Speaking at Davos in 2026, he warned:

“Capital wars could follow Trump’s actions with countries dumping US assets”

I read that as a description of escalation risk. In a world where assets can be frozen and payment rails can be politicized, selling U.S. assets becomes a strategic act, not merely a portfolio rebalance.

Financial sanctions were meant to punish adversaries but may have accelerated the dollar’s decline by incentivizing alternatives. Defensive actions can have offensive consequences. If you show the world that reserves can be immobilized, you also show the world why reserves should be held in something harder to immobilize.

Gold fits that need. It is boring. It is heavy. It is politically awkward. And it is, in a certain sense, the only reserve asset that doesn’t require someone else’s permission.

Which brings me back to the person checking their brokerage account and wondering how any of this touches them.

It touches them through the quiet mechanics of devaluation.

The Quiet Confiscation

I think the most important feature of devaluation is that it can happen without being experienced as an event.

When a government taxes you directly, you feel it. When a government cuts benefits, you feel it. When the currency buys less over time, you tend to blame “prices,” “corporate greed,” “supply chains,” or some vague sense that the world is getting more expensive. The politics of it are convenient precisely because causality is diffuse.

That’s why nominal gains are such an effective anesthetic. If your portfolio is up 18% and your lifestyle feels 10% more expensive, you can still tell yourself you’re ahead. But if the measuring stick is moving faster than your assets, you’re losing ground while feeling fine.

The Federal Reserve’s institutional design reinforces this incentive structure. The Fed prioritizes “price stability and maximum employment” as its dual mandate. That mandate creates a constant pressure to smooth downturns, support employment, and prevent deflationary spirals. In practice, when crises hit, the bias is toward liquidity and stabilization. The political system punishes unemployment quickly. It rarely punishes long-run currency dilution with the same urgency.

Gold’s behavior over time captures that cycle. Long-term market data shows how post-2008 quantitative easing coincided with gold rising from about $800/oz to $1,900/oz by 2011, then falling sharply as hyperinflation fears eased, until 2020 money printing revived prices. That arc matters because it shows two truths at once: gold can respond powerfully to monetary expansion, and gold can also crash.

Gold might continue outperforming, or it might repeat the 2011 to 2015 experience and fall hard. What would resolve that isn’t a slogan. It’s the interaction between real rates, liquidity conditions, and how credible the monetary regime feels when stress hits. Gold isn’t a one-way bet. It’s a barometer that can overshoot.

Still, the longer historical pattern is hard to ignore. Gold outperformance preceded major dislocations: the 1930s Great Depression, 1970s stagflation, the 2000 dot-com bust, the 2008 financial crisis, and the 2020 pandemic. That’s pattern recognition. When gold starts beating paper claims in a sustained way, it often means the system is pricing in stress before the public narrative catches up.

The beauty of devaluation, from a policymaker’s perspective, is that it’s a wealth transfer that doesn’t require a formal announcement. It shifts purchasing power from savers to debtors. It makes old debts easier to carry. It reduces the real value of promises. And because most people measure success nominally, it can be sold as prosperity.

The S&P’s “good year” against the dollar and “bad year” against gold is a case study in how a society can feel richer while becoming poorer in real terms.

So what does it mean, concretely, to live in that gap?

What It Means, Who It Pressures, and What I’m Watching

When I put the pieces together, I see a system responding to constraints.

The gap between nominal returns and real purchasing power functions like a wealth transfer from savers to debtors, and the U.S. government is the largest debtor. In a high-debt world, a modest amount of currency devaluation can do what tax hikes and spending cuts can’t: it can stabilize the real burden of obligations without forcing a political coalition to openly vote for pain.

Central bank gold buying matters because the institutions closest to sovereign risk are repositioning toward an asset that doesn’t depend on the credit or goodwill of another sovereign. They’re doing it while many of them still publicly affirm the stability of the existing system. That contradiction is a signal.

Who benefits in this environment? Entities with hard assets and real productive capacity, and countries building alternative financial infrastructure that reduces their vulnerability to sanctions and payment chokepoints. Anyone who insists on measuring wealth in purchasing power rather than nominal units will detect erosion earlier.

Who gets pressured? Savers in dollar-denominated assets that don’t adjust quickly, holders of long-duration fixed claims, and retirees relying on purchasing power stability rather than nominal account growth. If your wealth is primarily a claim on future currency that can be created at will, you’re exposed to policy choices that don’t require your consent.

There are real uncertainties:

Whether the BRICS “Unit” moves from pilot to operational remains genuinely unclear. A pilot can stay a pilot. But if it becomes operational at scale, it would mark a structural shift in settlement behavior.

The timing of any currency crisis or acceleration is unknowable in advance. Markets can tolerate imbalances longer than skeptics expect, and being early is indistinguishable from being wrong for long stretches.

Whether gold continues to outperform or crashes again is also uncertain, as history already demonstrated in the 2011 to 2015 period.

I do, however, have tripwires that would change my view:

Sustained dollar strength against gold for 12+ months. If gold weakens materially while the dollar strengthens, it suggests the devaluation impulse is not the dominant force, at least for a time.

Central banks reversing course and selling gold reserves. If the WGC data starts showing sustained selling, it would imply that the institutional fear trade is fading.

A credible path to reducing U.S. debt-to-GDP without currency devaluation. If the U.S. materially improves its trajectory through growth, fiscal reform, or some combination that doesn’t rely on dilution, the whole framework needs updating.

Until those tripwires trigger, I’m watching:

The S&P-to-gold ratio. Further compression suggests continued real wealth erosion even if stocks rise nominally.

The pace of central bank gold buying. Acceleration would signal intensifying institutional concern.

Whether BRICS settlement efforts move from pilot to operational in a way that changes trade invoicing and reserves.

Treasury auction demand, especially foreign participation, as a real-time referendum on dollar assets.

The refinancing path after the $9.2 trillion maturity wall in 2025, and what rates future maturities roll into.

The ruler is shrinking. The question is whether you notice before it’s too late to matter.

Interesting framing. Measuring equities in gold is a useful way to surface “unit of account” risk that nominal statements can hide. I’d only add this isn’t automatically an anti-equity conclusion, it’s a reminder the regime is increasingly about what you measure wealth in. Also, not all equities are equal here: the parts of the market tied to AI bottlenecks (compute, power, grid, critical inputs) have held up well, and if the capex wave persists they may keep doing the heavy lifting. Central bank gold buying reads like a quiet vote for resilience and optionality.

This is incredibly well argued! The shrinking ruler concept really hits diffrent when you see those S&P-to-gold ratios over time. I've been watching my retirement account grow nominally but feeling like everything costs more, and now I get why. The part about central banks doubling thier gold reserves while publicly supporting dollar stability feels like the biggest tell.