The $100 Billion AI Bailout Nobody's Calling a Bailout

62% of companies see zero productivity gains from AI. Private credit is imploding. And the biggest funding round in tech history just became a rescue operation.

OpenAI is in talks for a $100 billion funding round. The same week, Apollo wrote down $170 million in private credit to zero. Microsoft disclosed that 45% of its $625 billion in remaining performance obligations comes from a single customer: OpenAI. And buried in survey data from Apollo’s own research team, a number that explains all of it: 62% of firms report no change in labor productivity from AI.

The money is still flowing in at a scale that would’ve sounded absurd two years ago. The productivity gains that were supposed to justify that money, at least in the enterprise, aren’t showing up with anything like the same force.

That’s the contradiction I can’t get past. This isn’t a story about AI “losing momentum” culturally. Interest is still intense. Executive attention is still intense. Capital commitments are still enormous. It’s a story about something more prosaic and more dangerous: the gap between adoption and results.

When that gap persists, it doesn’t just create disappointed CIOs. It creates renewal risk. It creates cash burn that can’t be refinanced on friendly terms. And it creates a specific kind of fragility in the market that financed the buildout: private credit, which grew into a multi-trillion-dollar pillar of modern capitalism while public markets were still arguing about whether AI was a feature or a fad.

The cracks aren’t all in one place. They’re appearing where you’d expect a feedback loop to form: adoption flattening, productivity not compounding, credit marks getting uglier, and the biggest AI players quietly trying to buy themselves time.

The S-Curve Flattens

The first thing I did was stop listening to the hype and look for the shape of the curve.

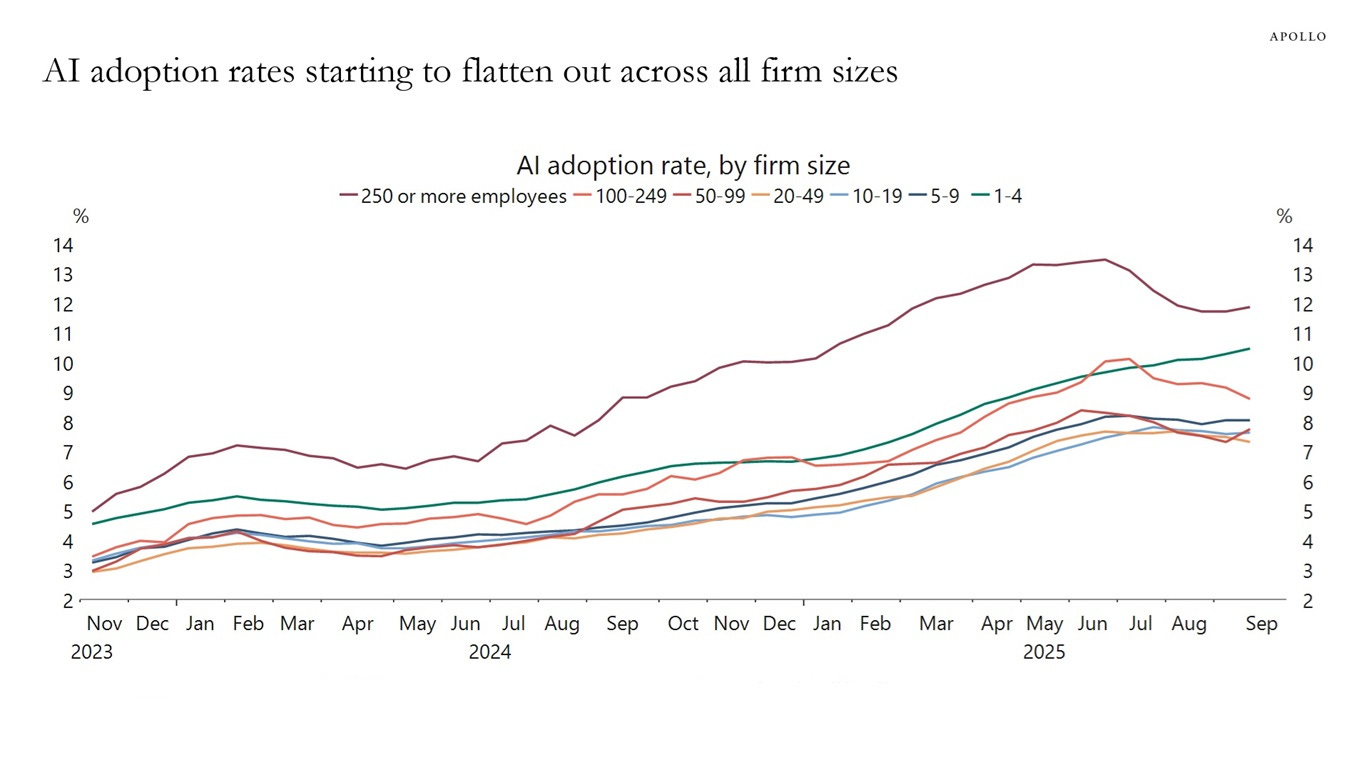

Apollo Academy’s tracking of enterprise behavior is blunt about what’s happening. In a November 2025 research report, Apollo’s chief economist described the pattern in plain English: “AI adoption starting to flatten out across all firm sizes” in the Apollo Academy report.

That phrase matters because it’s not saying “adoption is low.” It’s saying adoption is stalling. Those are different diagnoses. Low adoption can be fixed with evangelism, better UX, lower prices, or a killer use case. A flattening curve usually means the early adopters have adopted, the late adopters have experimented, and the marginal buyer is asking a harder question: what did we actually get for this?

This is the classic S-curve problem. Early adoption is fast because the first cohort is self-selected: they have the budget, the appetite for experimentation, and the internal champions. Then euphoria sets in, because the early cohort becomes proof that “everyone is doing it.” And then the curve slows because the next cohort doesn’t have the same conditions, or doesn’t see the same returns.

The more interesting detail in Apollo’s work isn’t that firms are trying AI. It’s what happens after they try it.

In Apollo Academy’s January 2026 productivity analysis, the headline statistic is devastating to the “inevitable productivity boom” narrative: 62% of firms report no change in labor productivity from AI, as laid out in the Apollo Academy productivity report. Nearly two-thirds. Not “small gains.” Not “gains but hard to measure.” No change.

If you’re a CFO, that’s the statistic that turns AI from a strategic initiative into a procurement line item that needs justification.

Apollo’s report also quantifies something that’s easy to miss if you only look at adoption headlines: the time savings from generative AI in the workplace aren’t compounding yet. They’re wobbling. Apollo found that GenAI time savings peaked at 1.8% of hours worked in November 2024 and dipped to 1.7% by August 2025, in that same Apollo Academy report.

A tenth of a percentage point sounds trivial until you remember what’s supposed to be happening in the bull case. The bull case isn’t that GenAI saves a sliver of time for a sliver of tasks. The bull case is that it starts as a sliver and then scales, spreads, and compounds as workflows get rebuilt around it. A peak-and-dip pattern suggests something else: experimentation that hits friction, or novelty that wears off, or implementation that doesn’t translate into durable process change.

McKinsey’s survey work corroborates the same tension from a different angle. In its State of AI reporting, McKinsey found 88% AI adoption, but noted that most companies “have not yet begun scaling,” and that 39% report less than 5% EBIT impact.

Put those together and you get a picture that feels less like a revolution and more like a corporate holding pattern. Adoption is widespread, but scaling is limited. Measurable profit impact is modest for a large share of adopters. Labor productivity, for most firms, hasn’t changed.

This is where the story gets uncertain in a way that matters. It’s genuinely possible that productivity gains are lagging and will materialize later, once companies do the hard work of redesigning processes and governance. It’s also possible that the gains are real but captured in ways that don’t show up as “labor productivity” yet: better quality, faster cycle times, fewer errors, more output that gets reinvested into growth rather than cost reduction.

But even if you grant all of that, the immediate market consequence is the same. A flattening adoption curve plus unclear productivity gains creates a specific corporate behavior: slow down new spending and scrutinize renewals.

And that’s where the capital stack starts to matter.

If adoption is flattening because productivity isn’t materializing, what happens to the capital that funded the buildout?

Private Credit Starts to Crack

The AI buildout wasn’t financed only by venture capital and public equity exuberance. A meaningful share of the real-world infrastructure and corporate leverage behind it sits in private credit, a market that ballooned in the low-rate era and then tried to normalize itself in a higher-rate world without admitting how much refinancing risk it had embedded.

The scale is the first thing to internalize. Chronograph’s analysis of the market’s expansion describes private credit growing from roughly $300 billion in assets under management in 2010 to $1.6 trillion by 2023, and estimates ranging from $1.7 trillion to $3 trillion by early 2025, as detailed in Chronograph’s write-up. A 5-to-10x expansion in about 15 years doesn’t just create a new asset class. It creates a new systemic dependency.

Then you look at how directly that capital has been pulled into AI infrastructure.

Meta’s October 2025 arrangement with Blue Owl is a clean example because it’s explicit: Blue Owl agreed to finance the development of Meta data centers in a deal described as $27 to $30 billion, according to Meta’s own announcement on the Hyperion data center development. This is private credit stepping into a role that used to be dominated by public debt markets and bank syndicates.

When people talk about “AI capex,” they often picture hyperscalers writing checks from operating cash flow. That’s part of it. But deals like Meta-Blue Owl show how the financing ecosystem has adapted: private lenders funding long-duration infrastructure tied to the AI narrative.

Now layer in the stress signals.

On January 26, 2026, Bloomberg reported that Apollo wrote down $170 million in private credit to zero, in a loss on an asset-backed loan that had been deemed protected. A write-down to zero is not a gentle mark. It’s an admission that the recovery value is, for practical purposes, gone.

It wasn’t isolated. In the fourth quarter of 2025, the BlackRock BDC marked down NAV by 19%, according to Private Debt Investor. A 19% NAV markdown is the kind of move that forces uncomfortable conversations with allocators, not just internal risk committees.

And then there’s the flow data, which is where sentiment becomes behavior. A market analyst posting under the handle @junkbondinvest summarized what they saw as a turning point: “$7bn pulled from private credit Q4...PC eating reputational hit” in a post on X dated January 17, 2026. The key isn’t the phrasing. It’s the claim of $7 billion pulled from private credit in Q4 2025, which aligns with the broader theme: investors don’t need a full-blown crisis to start backing away. They just need enough marks, enough headlines, and enough uncertainty about what’s really inside the vehicles.

The honest answer is that nobody knows yet how much of this stress is AI-related versus a broader consequence of higher rates, refinancing pressure, and the natural end of the “everything can be privately financed forever” era. That uncertainty matters because it changes the story’s mechanism.

If private credit is cracking primarily because of AI concentration, then the feedback loop is tight: adoption flattening weakens AI cash flows, which weakens credit, which tightens funding, which slows buildout, which further pressures adoption narratives.

If private credit is cracking for broader reasons, then AI may be more of a passenger than a driver. The loop still exists, but it’s looser and more contingent.

What I can say with confidence is simpler: the timing is bad. AI is still in its capital-intensive phase, and private credit is showing signs of stress at the same time. That’s how funding regimes change: not when the story dies, but when the financing gets picky.

And the pattern I keep seeing is this: each failure is treated as idiosyncratic until the accumulation forces the market to admit it’s systemic. It’s just how credit narratives work.

PIMCO sees this coming. And they’re warning their clients.

The Smart Money’s Warning

When a firm like PIMCO starts flagging hazards in an asset class, I pay attention less to the rhetoric and more to the institutional incentive structure. Big managers don’t usually lead with alarm. They lead with positioning. Warnings tend to arrive when risks have matured enough that not warning becomes reputationally dangerous.

PIMCO’s own materials put its scale at $2.3 trillion in assets under management, in its 2026 outlook. That doesn’t make it infallible. It does make it plugged in.

In that same outlook, PIMCO warns about private credit’s hidden hazards: refinancing risks from zero-rate era loans coming due, sector concentration in AI, and the structural issue that private credit often has limited disclosure and limited mark-to-market discipline.

The key here isn’t that PIMCO is bearish. The key is that PIMCO is describing the exact conditions under which a financing loop breaks: loans originated under one rate regime, borrowers dependent on growth narratives, and investors who don’t get clean price signals until the marks finally move.

So private credit is stressed and adoption is flattening. What does that mean for the companies at the center of the AI buildout?

Microsoft’s OpenAI Problem

Microsoft is the most important corporate “tell” in this entire story because it sits at the junction of enterprise adoption, cloud infrastructure, and the flagship AI partnership that has come to symbolize the boom.

In Q2 FY2026, Microsoft disclosed $625 billion in remaining performance obligations (RPO). RPO is not revenue today. It’s contracted future revenue not yet recognized. It’s one of the cleanest windows into how much business is already “booked” and how concentrated that booking might be.

Here’s what matters. On the Q2 FY2026 earnings call, Microsoft disclosed: “Approximately 45% of our commercial RPO balance is from OpenAI”, as captured in the earnings call disclosure.

CloudWars did the arithmetic: 45% of $625 billion is roughly $281 billion, and framed it as an OpenAI commitment driving the surge in RPO.

I want to pause on that number because it’s easy to read past it. $281 billion is not a partnership. It’s not a strategic bet. It’s a concentration event.

At the same time, Microsoft’s core business is still growing. CNBC reported Q2 FY2026 revenue of $81.3 billion, up 17% year over year, in its coverage of the earnings report. Yet the stock fell post-earnings, a tension that tells you the market is looking through current revenue and focusing on something else.

The simplest explanation is that markets are forward-looking and don’t like concentrated exposure to a customer whose economics are still unsettled. If nearly half of your contracted future revenue is tied to one counterparty, investors start asking questions that don’t show up in headline growth rates.

This is where the adoption plateau shows up as a balance-sheet issue.

Microsoft’s enterprise AI push, including Copilot, is often sold in seat-based terms: per-user pricing, adoption targets, renewals. The risk in that model is not that companies won’t try it. The risk is that they try it, don’t see enough productivity impact, and then treat renewal as optional.

The renewal cycle matters because a lot of enterprise software is sold on multi-year contracts. If you sold aggressive AI bundles in 2023 after the GPT integration wave, the renewal window starts to come due in 2026 and 2027. That’s exactly when Apollo’s data suggests productivity gains are not yet convincing for most firms.

I’m not claiming Copilot renewals will collapse. The honest answer is that nobody knows yet. But the mechanism is straightforward: if AI doesn’t change labor productivity for most firms, then “AI seats” become a cost to be optimized, not a capability to be expanded.

And if OpenAI is the single largest driver of Microsoft’s RPO concentration, then OpenAI’s funding and burn rate stop being Silicon Valley gossip and start being a material risk factor for a $3 trillion-class public company.

Which brings us to what OpenAI actually needs to survive.

The $100 Billion Bail-In

The number itself is the story: OpenAI is in talks for up to $100 billion in a funding round that would include Amazon, SoftBank, Nvidia, and Microsoft. The reported structure is striking: Amazon up to $50 billion, SoftBank $30 billion, Nvidia up to $30 billion, and Microsoft around $10 billion.

Even if the final terms shift, the direction is clear. This is not a “raise.” It’s a recapitalization of the AI frontier.

Then you look at OpenAI’s own projected economics. Yahoo Finance also reported that OpenAI forecasts a $14 billion loss in 2026 and does not expect profitability until 2029 at the earliest.

This is the capital intensity problem in its pure form: massive demand, massive compute needs, massive operating losses, and a business model that still depends on a productivity thesis that is not yet showing up broadly in the enterprise.

The part that made me sit up wasn’t even the burn. It was the way the infrastructure layer is starting to look like it needs backstops.

CoreWeave is a key infrastructure provider in the AI stack and serves OpenAI. CNBC reported that CoreWeave stock had dropped 64% from its high by December 2025.

Then, on January 26, CNBC reported that Nvidia invested $2 billion in CoreWeave at $87.20 per share, again in that same CNBC report.

Suppliers don’t usually need to backstop their customers. When they do, it suggests the demand chain is more fragile than the headline numbers imply. Nvidia has every incentive to keep the AI compute ecosystem liquid and expanding. But that’s exactly why this is such a revealing event: it looks like a strategic investment, but it also reads like a form of stabilization.

This is where the story gets murky in a way that matters. Nvidia’s investment could be interpreted as opportunistic, as strategic, or as defensive. It could be all three. The key point is that it exists at all, at this scale, in this moment.

Now connect the beats. OpenAI needs up to $100 billion more capital. OpenAI expects a $14 billion loss in 2026 and profitability no earlier than 2029. A major infrastructure provider in the chain saw a sharp drawdown. Nvidia steps in with $2 billion at a stated price.

That’s not the posture of an industry that has fully escaped the “subsidized growth” phase. It’s the posture of an industry still buying runway.

xAI shows the same pattern, with an additional wrinkle.

xAI and the SpaceX Escape Hatch

If OpenAI is the flagship of the AI frontier, xAI is the reminder that the frontier isn’t a single company. It’s a category of firms with similar economics: enormous compute needs, rapid scaling ambitions, and a constant search for capital that doesn’t come with suffocating terms.

In January 2026, Tesla announced a $2 billion investment in xAI, as reported by Teslarati. The related-party nature of that capital flow is the point. It’s not just “AI raising money.” It’s profitable or liquid adjacent entities being used to finance an AI buildout.

Then came the more revealing rumor: xAI was in talks for a SpaceX merger as a route to IPO liquidity, according to TechCrunch’s reporting. Whether or not that specific structure happens, the impulse is legible: find a liquidity escape hatch that doesn’t require the standalone AI economics to be fully proven right now.

Elon Musk’s public framing stayed in builder mode. On January 29, 2026, he posted: “Much more coming out from @xAI. We are cooking hard on many projects”.

I don’t read that as deception. I read it as the cultural truth of AI right now: the engineering pace is real, the ambition is real, and the product surface area is expanding fast. The financial reality can still be harsh underneath.

The pattern I keep seeing is that frontier AI companies are trying to finance themselves the way capital-intensive industries always do: by leaning on deeper-pocketed partners, by finding ways into public-market liquidity, or by attaching themselves to cash-generative businesses that can subsidize the burn.

Not everyone is in this position. Meta shows a different model.

The Meta Exception

Meta is spending like an AI frontier company, but monetizing like an incumbent with a built-in tollbooth.

Reuters reported that Meta guided 2026 capital expenditures to $115 to $135 billion, with a midpoint of $125 billion, as part of its “superintelligence push”. That capex number is so large it almost stops functioning as a corporate metric and starts functioning as industrial policy.

But Meta’s AI economics are structurally different from seat-based enterprise AI. Reuters also reported that Meta’s AI work has been tied to measurable performance improvements: conversion rates up 3% to 24% year over year, and watch time up 30%.

The distinction that matters here is what I think of as AI wrappers vs. AI enhancers.

Wrappers sell AI as a product layer that requires customers to adopt new workflows. The revenue depends on seats, renewals, and ongoing willingness to pay for a capability that may still feel experimental. If productivity gains are unclear, the customer can decide the wrapper is optional.

Enhancers use AI to improve an existing product that already has distribution and monetization. The customer doesn’t need a new workflow. The customer just experiences a better outcome inside a system they already pay for.

Meta’s core business is advertising. Advertisers don’t need to “adopt AI” as a workflow. They buy outcomes. If Meta’s feed gets more accurate and conversions improve, the monetization can show up transactionally, not as a seat renewal debate.

That’s why Meta can justify $125 billion in capex in a way that a pure-play AI vendor can’t. It’s not because Meta is more visionary. It’s because Meta’s AI spending is tied to an engine that already prints cash and can measure lift.

This doesn’t mean Meta is risk-free. Massive capex always carries execution risk. But it does mean Meta’s AI bet is less exposed to the specific failure mode Apollo’s data is hinting at: broad enterprise adoption without broad productivity gains.

Which brings us back to the central question.

What It Means

When I line up the adoption data, the productivity surveys, the credit stress signals, and the funding headlines, I keep coming back to a single mechanism: AI is entering the phase where capital intensity meets productivity reality.

The boom doesn’t need to “end” for the loop to crack. It just needs to become more selective.

Here’s the loop as I see it. AI vendors and frontier labs require enormous capital to fund compute, talent, and infrastructure. OpenAI’s reported talks for up to $100 billion, paired with its projected $14 billion loss in 2026 and profitability no earlier than 2029, are the cleanest expression of that reality.

Enterprises adopt AI widely but don’t yet see broad productivity gains. Apollo’s finding that 62% of firms report no labor productivity change, and the slight dip in GenAI time savings from 1.8% to 1.7%, suggests the gains aren’t compounding fast enough to make budgets feel inevitable.

Renewal risk rises for seat-based AI models. If the ROI is ambiguous, CFOs treat AI seats like any other software line item. They renegotiate, downsize, or delay scaling. This is where the S-curve flattens.

Funding markets start to care about cash flows again. Private credit stress, write-downs, markdowns, and outflows don’t need to be “caused by AI” to matter. They tighten the environment at the exact moment AI companies still need abundant, patient capital.

The infrastructure layer gets pulled into stabilization behavior. Nvidia investing $2 billion in CoreWeave after a sharp drawdown is the kind of move that makes sense in a fragile ecosystem: protect the demand chain, protect the platform, protect the narrative.

The uncertain part is causality. It’s genuinely unclear how much private credit stress is directly tied to AI concentration versus broader refinancing and valuation pressures. It’s also genuinely unclear whether productivity gains will show up with a lag as firms learn to scale and redesign workflows. And it’s unclear whether OpenAI’s $100 billion round closes and on what terms, which will determine how long the frontier can keep running at today’s burn rate.

But I don’t need certainty on those unknowns to identify the pressure points investors should be watching.

What I’m watching is where the loop would either heal or break.

Enterprise AI productivity surveys matter. A major shift would be if something like Apollo or McKinsey shows 40% or more of firms reporting meaningful productivity gains by the end of 2026. That would change the renewal math.

Private credit marks and flows through 2026 matter. Stabilization in flows and fewer ugly write-down headlines would suggest the financing regime can keep supporting AI capex without a broader repricing.

Whether OpenAI’s $100 billion round closes, and at what terms matters. A clean close would extend runway. Harsh terms would reveal how much bargaining power capital now has.

Microsoft’s Copilot and seat-based renewal dynamics as 2023-era contracts come due in 2026 and 2027 matter. If renewal rates are above 80%, the “wrapper” model looks more durable. If they’re weak, the adoption plateau becomes a revenue problem.

Infrastructure counterparties like CoreWeave matter. Not because one company defines the ecosystem, but because infrastructure is where cash flow reality tends to surface first.

In this environment, I think the winners and losers will be separated less by who has the best demo and more by who has the best economic shape.

Who benefits are the firms using AI to enhance existing revenue streams rather than selling AI as a standalone product. Firms with balance sheets that don’t require continuous capital infusion. And infrastructure plays that have locked in long-term contracts rather than depending on fragile counterparties.

Who gets pressured are AI companies dependent on seat renewals amid productivity doubts, private credit funds with concentrated exposure to AI-linked borrowers, and any firm in the chain that requires the productivity thesis to be true on a near timeline to keep refinancing cheap.

The $100 billion round and the 62% no-productivity-change figure can coexist for a while. Capital can flow to things that aren’t working yet, especially when the strategic stakes feel existential. But the gap between investment and return has to close eventually.

Either productivity materializes, or the capital stops flowing.

The private credit market is starting to vote on which way this goes.